Do LLMs Have Utility Functions?

Insights from choice experiments with financial portfolios.

Samford University

Western University

Introduction

LLMs as Economic Actors

Do LLMs need a utility function?

- AI agents are being deployed as autonomous decision-makers.

- These models are increasingly responsible for evaluating economic tradeoffs.

- Knowing how economic tradeoffs are evaluated becomes critical for alignment.

- However, the underlying preferences of these models remain largely unmapped.

Do LLMs adhere to the rationality axioms of utility theory?

Each principal deploying AI agents will want to understand their preferences, and potentially engineer alignment with the principal's preferences.

How LLMs Work

Choices from Autoregressive Distributions

How LLMs Generate Text

- $\tau$: temperature is the scale of the stochastic component.

A Typical Choice Experiment Prompt

Choose the portfolio you prefer and reply with A or B only.

Option A offers an expected return of 8% and

a standard deviation of 12%.

Option B offers an expected return of 10% and

a standard deviation of 5%.

The Core Insight

The LLM's choice mechanism is McFadden (1974)'s conditional logit.

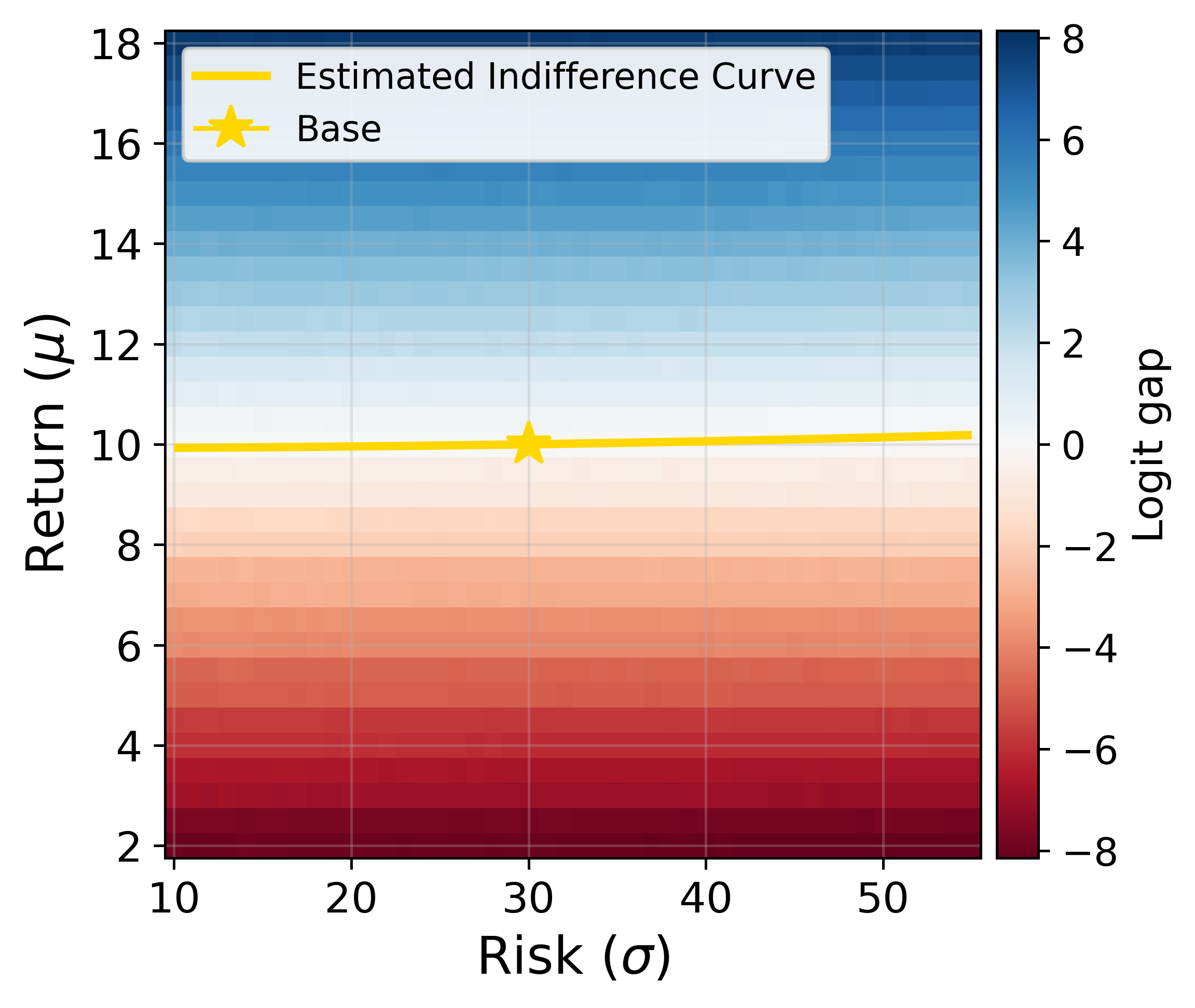

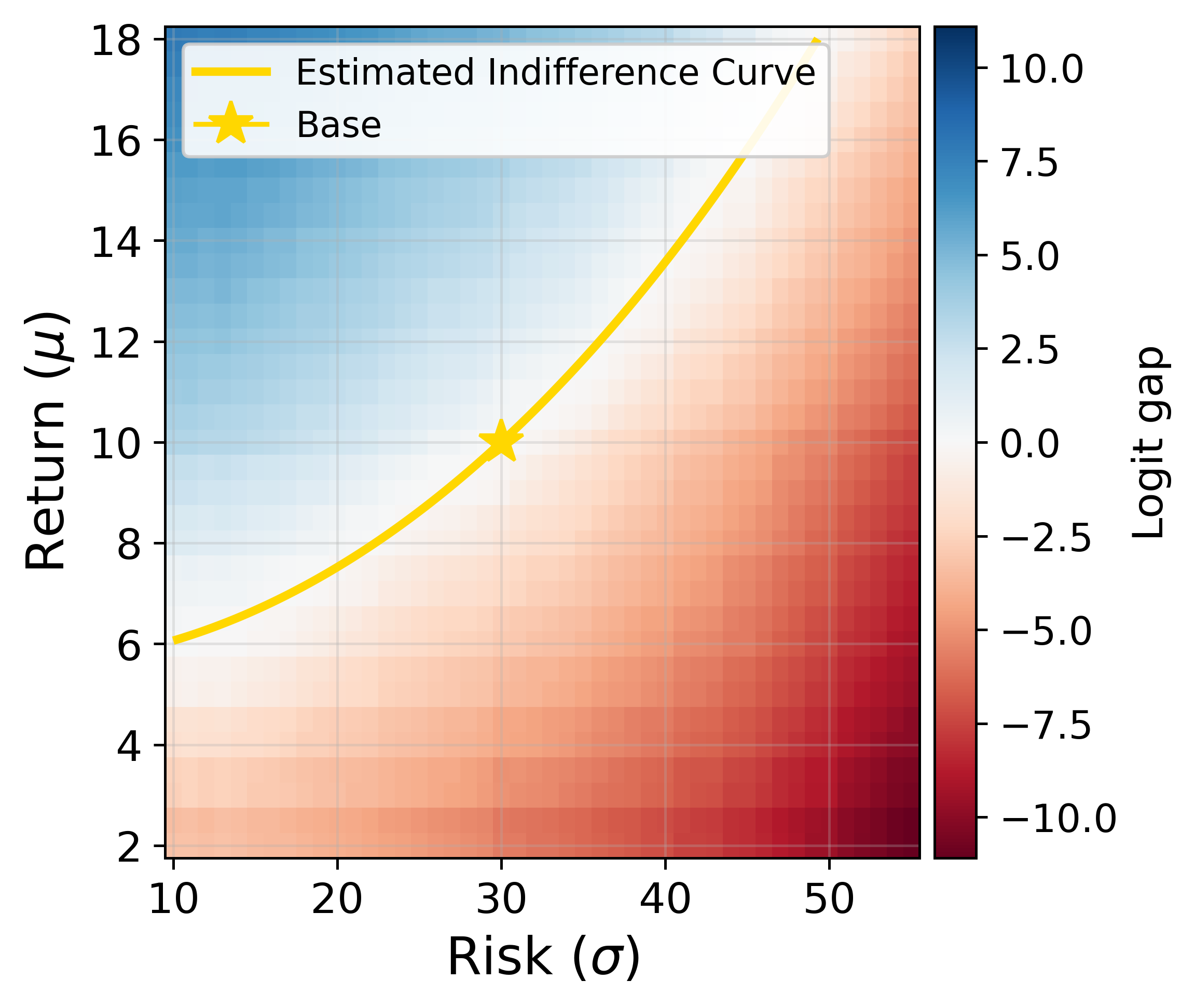

Llama 3.1 8B Indifference Curve

Utility Axioms

Testing the Economic Rationality of LLMs

Utility Axioms

Complete: must express some preference or indifference.

The probability of selecting a choice label among the available options will be approximately 1.

\( P(A \mid x, \tau) + P(B \mid x, \tau) \approx 1 \)

Utility Axioms

Reflexive: any bundle of goods is at least as good as itself.

When options are identical, their probability of selection will be the same.

\( P(A \mid x, \tau) = P(B \mid x, \tau) \)

Utility Axioms

Continuity: there is a "tipping point" between being better than and worse than a given option.

Let $A\succ B\succ C$. There is a value $\epsilon\in [0,1]$ such that

\( (1-\epsilon)P(A \mid x, \tau) + \epsilon P(C \mid x, \tau) \)

\( = P(B \mid x, \tau) \)

Utility Axioms

Strong monotonicity: more (less) of a good (bad) is always better.

The probability of selecting a dominant option will always be higher than a non-dominant one.

\( P(A \mid x, \tau) > P(B \mid x, \tau) \)

Utility Axioms

Transitive: if $A\succ B$ and $B\succ C$, then $A\succ C$.

The probability of selecting A will always be higher than B, and B higher than C.

\( P(A \mid x, \tau) > P(B \mid x, \tau) \)

\( P(B \mid x, \tau) > P(C \mid x, \tau) \)

Experimental Design

A portfolio choice laboratory and a structural model of risk preference.

Portfolio choice laboratory

Binary menus over risky assets with known payoff moments.

Choose the portfolio you prefer and reply with A or B only.

Option A offers an expected return of [\(\mu_A\)]% and a standard deviation of [\(\sigma_A\)]%.

Option B offers an expected return of [\(\mu_B\)]% and a standard deviation of [\(\sigma_B\)]%.

Results

Rationality diagnostics, and inducing specific preferences.

Rationality diagnostics: Open Weight Models

Do LLMs satisfy the axioms of choice over risky portfolios?

| Model | Complete | Reflexive | Continuity | Monotonicity | Transitive |

|---|---|---|---|---|---|

| Qwen 3 (14B) | 0.9999 | 0.0002 | 1.0000 | 1.0000 | 0.9749 |

| Qwen 3 (8B) | 0.9999 | 0.0018 | 1.0000 | 1.0000 | 0.9923 |

| Gemma 4 (31B Instruct) | 0.9999 | 0.0000 | 1.0000 | 1.0000 | 0.9882 |

| Ministral 3 (8B Instruct) | 0.9995 | 0.0496 | 0.9667 | 1.0000 | 0.9643 |

| Gemma 2 (9B Instruct) | 0.9960 | 0.5236 | 1.0000 | 1.0000 | 0.9238 |

| Llama 3.1 (8B Instruct) | 0.9021 | 0.9250 | 1.0000 | 1.0000 | 0.9851 |

| Llama 3.1 (70B Instruct) | 0.7580 | 0.0648 | 1.0000 | 1.0000 | 0.9562 |

| Llama 3.1 (8B Fine-Tuned) | 0.9977 | 0.9966 | 1.0000 | 1.0000 | 0.9994 |

Rationality diagnostics: Frontier Models

Do frontier models satisfy the axioms of choice over risky portfolios?

| Model | Complete | Reflexive | Continuity | Monotonicity | Transitive | IIA |

|---|---|---|---|---|---|---|

| Claude 4.5 Haiku | 0.970 | 0.072 | 1.000 | 1.000 | 0.857 | 0.498 |

| Claude 4.6 Sonnet | 0.964 | 0.000 | 1.000 | 1.000 | 1.000 | 0.503 |

| GPT-4o | 0.998 | 0.009 | 1.000 | 1.000 | 1.000 | 0.301 |

| GPT-4o Mini | 1.000 | 0.008 | 1.000 | 1.000 | 1.000 | 0.586 |

| Gemini 2.5 Flash Lite | 1.000 | 0.000 | 1.000 | 1.000 | 0.987 | 0.802 |

Fine-tuning Preferences

Conclusion

Contributions, limitations, and implications for agentic AI deployment.

Contributions & implications

- Formal equivalence between LLM softmax and the RUM. This places language model choice inside structural discrete choice methods, enabling recovery of cardinal utility indices directly from a model's single token logit outputs over choices.

- Experiments support the existence of a utility function. The results on our five axiom measures indicate the existence of a utility function over risky portfolios.

- Specific preferences can be induced via fine-tuning. Existing alignment pipelines allow for us to engineer the preferences of LLMs in a targetable way.

To deploy agentic AI, the models must be economically coherent and internally consistent. We show preferences governing their behaviour can be measured and targeted.

Thank you.

Fin.

Samford University

Western University

LLMs Live in Plato's Cave, We Project the Shadows

LLMs Are Ideal Experimental Subjects

- Environmental control for ceteris paribus variation.

- AIs are cheap and fast.

- AI never gets tired of answering your questions.

- Every simulation is "real" to the AI.